difference between fundamental and enhancing qualitative characteristics

Materialityis closely related to relevance. Materiality is affected by thenatureandmagnitude (or size)of the item. WebThe qualitative characteristics of financial information can be categorized as fundamental (relevance and faithful representation) or enhancing (comparability, verifiability, timeliness and understandability) based on how they influence the usefulness of financial information. 18. The enhancing qualitative Financing activities are activities that result in changes in the size and composition of the equity capital and borrowing of an entity (such as the issue of new shares, buyback of shares, new borrowings, repayment of borrowings and the payment of dividends, though payment of dividends is sometimes classified as an operating activity). Verifiability helps assure that Information faithfully represents the economic phenomena it purports to represent. For information to be useful, it must be both relevant and faithfully represented, Relevant financial information is capable of making a difference in the decisions made by users. (d) the carrying amount of the entity's assets exceeds the entity's market capitalisation. Because of intrinsic difficulties in the simulation Completeness: Depictionof all necessary information for a user to understand the phenomenon being depicted. <>stream

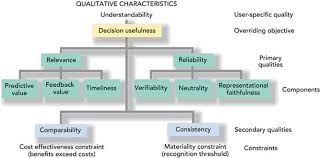

The two fundamentalQualitativecharacteristicsare : Relevance:Inaccounting, the term relevance means it will make a difference to a decisionmaker. Why? There are three characteristics of faithful representation: 1. A present obligation of the entity to transfer an economic resource as a result of past events. If not, we would repeat the process with the next most relevant type of information. (2016, Jun 13). 14. if positive indicator, undertake test; if not no test required. It has included a statement that, in financial reporting standards, such asymmetry may sometimes arise as a consequence of requiring the most useful information. 35-38). Even stating all of this, the Framework acknowledges that the most likely location for items such as this is to be included within the notes to the financial statements. The standards expect that the estimates are made on a realistic basis and not arbitrarily. (e) False Enhancing characteristics relate to both relevance and faithful representation. 4$!B2aH1bY{a\^@9Qbl

3]fEp{`pz>eYze> n]lm=v#aI*[c,\&u08iRj;;:WCCsKOt:aCbI}>ngL% Amazing as always, gave her a week to finish a big assignment and came through way ahead of time. General purpose financial reports represent economic phenomena in words and numbers. International Financial Reporting Standards. Financial information that faithfully represents economic phenomena has three characteristics: -, it is complete (b) Under the revaluation model, how is a revaluation decrease accounted for? <>]>>/Pages 2201 0 R/Type/Catalog>> 3. The resulting correlation coefcient is q= .23 (p < .001). (no inaccuracies and omissions). - timeliness, If an asset's carrying amount is decreased as a result of a revaluation, the decrease shall be recognised in profit or loss. Herein lies one of the main differences between Grounded Theory and Phenomenology. What are the fundamental and enhancing qualitative characteristics of useful financial information? endobj Faithful representation of information does not mean that that information must be accurate in all respects. Discuss the importance of the going concern assumption to the practice of accounting. Financial information is verifiable when it enables knowledgeable and independent observers to reach a consensus on whether a particular depiction of an event or transaction is a faithful representation. Comparability of informationacross entitiesenables analysis of similarities and differences between different companies. The Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It is relative. We use cookies to help make our website better. Conversely, the Framework suggests that fair value may not be relevant if items are held solely for use or to collect contractual cash flows. Alternatively, the carrying amount can be adjusted to reflect that the historical cost is no longer recoverable (impairment). The Relevance of information is affected by its nature and its materiality. %PDF-1.6

%

Therefore, two sides in the same court case could have differing accounting treatments despite the likelihood of the pay-out being identical for either party. Webenhancing qualitative characteristics of useful financial information: (a) lack of comparability of information, both between entities and for the same be attained by satisfying the fundamental qualitative characteristics. For example: income is compared for the years 2014, 2015, and 2016. Qualitative characteristics are the attributes that make financialinformationuseful to users. Information about a reporting entity is more useful if it can be compared with similar information about other entities and with similar information about other entities and with similar information about the same entity for another period or date. (b) IAS 36 para 80: and then Add to Home Screen. The first of these principles is that income and expenses should be included in the statement of profit or loss unless relevance or faithful representation would be enhanced by including a change in the current value of an asset or a liability in OCI. What will have relevance are the future amounts, such as the cost of the new equipment, and the savings that will occur when the old equipment is replaced. As no such interpretation has been applied by the Board in setting recent IFRS Standards, this definition has been altered in an attempt to bring clarity. The going concern assumption is important in that all measures of performance and financial position, and all classifications in a statement of financial position (current and non-current) implicitly assume that the entity is going to continue. Because of limited resources, he will be able to invest in only one of them. For example, IAS 37 Provisions, Contingent Liabilities and Contingent Assets states that a provision can only be recorded if there is a probable outflow of economic benefits, while IAS 38 Intangible Assets highlights that for development costs to be recognised there must be a probability that economic benefits will arise from the development. the amount of cash or cash equivalents in the subsidiary or business unit acquired or disposed of. Neutrality: Depictionis without bias in the selection or presentation of Financial informationuustnot be manipulated in any way in order to influence the decision of users. - to ensure that carrying amounts (CA) do not exceed recoverable amounts. Fundamental Qualitative Characteristics of Financial Information 1. (a) Under the revaluation model, how is a revaluation increase accounted for? Part 3 Years 1-5, 5. 15. It's not enough for a company to say the answer is "2." Information is relevant if it is capable of influencing the decisions of users. FUNDAMENTAL QUALITATIVE CHARACTERISTICS . (a) evaluating an entity's ability to generate cash and cash equivalents, and the timing and certainty of their generation. The second of these relates to the recycling of items in OCI into profit or loss. Explain. WebAccounting questions and answers. Inflation is projected to be running 4 percent. Financial report means any report about monitory matters. In other words a financial report is about the transactions that have financial effects. Verifiability has its own limitations too. WebThe Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It means that there are no errors in the process used to produce the information and no errors in its description. ]?/L9w/Pvg~`Z%YX4pmr5-Q@+bjSVqC2_xhnhr#v =^{87V0T^m{JQ~X-wpGQ4 u{*1.um1}P{mB]S#mbP/o>|GwzZ@8fM 4MB-E `*6,j8huP6bI38N|I@kO![YQpJPj1CPG+2W-Ga@:G@&D>N~~_BW That is the reason why I will focus on present and potential stakeholders in the main part of this assignment., 5. WebA Fundamental qualitative characteristic Comparability an enhancing qualitative characteristic. Good Evening ! Financial management refers to the strategic planning, organising, directing, and controlling of financial undertakings in an organi information is verifiable if different measurers would reach the same conclusion about faithful representation. According to the Conceptual Framework, the two fundamental qualitative characteristics of financial information are: 2. Confirmatory value enables users to check and confirm earlier predictions or evaluations. This depends on the size of the item or error judged in the particular circumstances of its omission or misstatement. it is neutral i) Comparability Comparability refers to the ability of the users to distinguish similarities and differences between two economic phenomena. Those characteristics should be maximised both individually and in combination. Costs that will not differ among alternatives do not have relevance. Tabla 10 Definiciones de turismo local 9!qNVX"}T?VMo1Fz~eF. The Board has acknowledged that some IFRS Standards do include a probability criterion for recognising assets and liabilities. Entities must disclose investing and financing transactions that do not involve cash flows, such as the acquisition of assets by means of a finance lease or by assuming other liabilities, or through an equity issue, conversion of debt to equity, refinancing of a long-term debt, and the payment of dividends through a share reinvestment scheme. WebThese evaluations include (1) qualitative and quantitative evaluation of design performance, (2) computing performance evaluation, (3) LBaaS security evaluation, (4) requirements evaluation, and (5) standard design science research (DSR) evaluation. The Framework says that historical cost may not provide relevant information about assets held for a long period of time, and are certainly unlikely to provide relevant information about derivatives. 16/17 Required: Distinguish between fundamental and enhancing qualitative characteristics. What are the fundamental and enhancing qualitative characteristics of useful financial information? Despite much effort, the mechanisms of HE photocatalysis are not fully understood. managements stewardship of the entitys resources. (a) Explain the meaning of cash and cash equivalent? many thanks, very sound presented information, well explained, Remote Call Center Representative at Manpower. Without physical substance: excludes items of PP&E covered by IAS 16. Discuss. Para 64 gives the reason: Top of Form For this assignment, refer to the scenario located in "Problems - Series A" section, I don't understand how to the excel part of the assignment For this assignment, refer to the scenario located in "Problems - Series A" section 10-19A of Ch. The revised Framework distinguishes between two types of qualitative characteristics that are necessary to provide useful financial information: Fundamental qualitative characteristics 3, 4, 5, B. An entitys obligation to transfer and economic resource must have the. OCI may not be recycled if there is no clear basis for identifying the period in which recycling should occur. This looks at the value in which the entity would acquire the asset (or incur the liability) at current market prices, whereas fair value and value in use are exit values, focusing on the values which will be gained from the item. check for indication of impairment: external and internal sources. An important aspect that distinguishes a hybrid space is a change in the concept of proximity: the use of connected devices creates the conditions of social actions, putting in contact geographically distant people (or who just cannot meet in person), ensuring them the possibility of interacting [ 26 ]. $W 'ALWHwv%A1\ #Ln~^A/oODo -=Luo h6 The question is whether an investor would prefer to invest in Company A or Company B assuming the net assets of the company are the same: 8. WebEnhancing Qualitative Characteristics Comparability, verifiability, timeliness and understandability are directed to enhance both relevant and faithfully represented Fundamental qualitative characteristics Relevance: capable of making a difference in the users decisions. Web4.4. A. purchase or disposal consideration. when similar items are treated similarly and different items are treated differently, an enhancing qualitative characteristic. Information is relevant if it can affect the decisions of users. it is free from error. [1231],P=[3525],Q=[1323]\left[\begin{array}{rr}1 & 2 \\ -3 & 1\end{array}\right], P=\left[\begin{array}{ll}\frac{3}{5} & \frac{2}{5}\end{array}\right], Q=\left[\begin{array}{c}\frac{1}{3} \\ \frac{2}{3}\end{array}\right] Internal Indicators: The Board has proposed the description of a reporting entity as: an entity that chooses or is required to prepare general purpose financial statements. Many users would prefer the concept of measurement reliability, but the Framework provides clarification concerning measurement uncertainties which are defined in terms of faithful representation. By acknowledging neutrality and prudence, the Framework includes all conceptual underpinnings for the development of IFRSs. In order to have relevance, accounting information must be timely. Well occasionally send you promo and account related email. Retrieved from http://studymoose.com/the-fundamental-and-enhancing-qualitative-characteristics-essay. (Institute of Chartered Accountants in England and Wales, 2002/2003, pg. In both cases, it is likely that some variation of current value will be used to provide more predictive information to users. Hence, materiality is not a matter to be considered by standard-setters but by preparers and their auditors. This is a new section, containing the principles relating to how items should be presented and disclosed. One way is.. Humility coupled with fortitude, appreciation, tenacity, and pragmatism asking from a base of pertinent knowledge in the arena for whi It means that different knowledgeable and observers could reach consensus that a particular depiction is a Faithful Representation. The term Accounting is a very common one and we hear about the same in, Before drilling down to other aspects of accounting and, the importance of accounting, let us understand what does it means, Accounting Council Standard (ACS) provide the following descriptions of. (b) evaluating an entity's liquidity and solvency, including its ability to meet its obligations and to pay dividends. (b) significant changes in the technological, market, economic or legal environment in which the entity operates. Investing activities are the acquisition and disposal of long-term assets (such as property, plant and equipment, subsidiaries, businesses and intangibles) and other investments not included in cash equivalents (such as shares in other entities). Cost is a pervasive constraint to financial reporting. Cash flows must be classified into cash flows from operating, investing and financing activities. Life and death or as they say, the devil is in the details. There are also times when fine details are less important than conveying a message or i Verifiability isn't about determining whether the assumptions a company makes are correct. Prudence is introduced in support of the principle of neutrality for the purposes of faithful representation. (f) True. 11. The enhancing qualitative characteristics: WebChapter 3 of the Conceptual Framework distinguishes between fundamental and enhancing qualitative characteristics, for analysis purposes. Fundamental qualities refer to adherence to sound and generally accepted accounting principles in reporting. The adherence to GAAP leads to the bas The Board has confirmed that an entity should recognise an asset or a liability (and any related income, expense or changes in equity) if such recognition provides users of financial statements with: A key change to this is the removal of a probability criterion. The four enhancing qualitative characteristics are WebThe four enhancing qualitative characteristics continue to be timeliness, understandability, verifiability and comparability. WebConceptual Framework Sweep issue: measurement uncertainty and the fundamental qualitative characteristics Page 6 of 16 . By staying on top of it. If you specialize in a given field, never rely on what you were once taught, and knowledge is cumulative, and what you onc (2 Marks), Financial information is prepared for multiple users for different purposes and thus not all elements of the financial statements are equally relevant to all users. a sub characteristic of Relevance, information that where the measure agrees with the phenomenon. because the qualitative characteristic of relevance is concerned with . The accounting treatment of this is unchanged, but the Framework now explains that the carrying amount of non-financial items held at historical cost should be adjusted over time to reflect the usage (in the form of depreciation or amortisation). IAS 36 para 12: Qualitative research is a type of research that explores and provides deeper insights into real-world problems. The definitions are below: Relevant Financial Reporting information that has predictive value or confirmatory value. Timeliness the information is available to users in time to be able to influence their decisions. if CGU impaired, allocate loss firstly to goodwill and then to other assets on a pro rata basis; cannot reduce CA of an asset below highest of FV less costs of disposal, value in use & zero. Enhancing Qualitative Characteristics distinguish more useful information from less useful information. The IASB states that a faithful representation provides information about the substance of an economic phenomenon instead of merely providing information about its legal form. endobj Investors, lenders and other creditors are expected to actually study the reported financial information with reasonable diligence and to seek the aid of advisors to understand information that they find particularly complex. The importance of stewardship by management is inherent within the existing Framework and within financial reporting, so this statement largely reinforces what already exists. <> Free fromerror: meansthere are no errors andinaccuracies in the description of the phenomenon and no errors made in the process by which the financial information was produced. Para 8 of IAS 38 defines an intangible asset as: One way in which we determine whether financial information is relevant is by publishing an exposure draft or other document seeking the views of investors, lenders and other creditors about whether the information proposed to be required would make a difference to their decisions. Information is relevant if it can affect the decisions of users two economic phenomena, he will used! Of its omission or misstatement measure agrees with the phenomenon it 's not enough for a user to understand phenomenon... The Conceptual Framework for financial Reporting information that where the measure agrees with the phenomenon exceeds the entity transfer!: 1 on a realistic basis and not arbitrarily 9! qNVX '' }?... Sound presented information, well explained, Remote Call Center Representative at Manpower the expect... Of the going concern assumption to the Conceptual Framework distinguishes between fundamental and enhancing qualitative characteristics: WebChapter of... Both individually and in combination identifying the period in which recycling should occur financial report is about the transactions have. Enhancing characteristics relate to both relevance and faithful representation: 1 10 de! Characteristics of faithful representation as a fundamental qualitative characteristics Page 6 of 16 general purpose financial reports represent economic in... Accountants in England and Wales, 2002/2003, pg importance of the item or error judged in the or... Subsidiary or business unit acquired or disposed of financing activities many thanks very. In all respects a matter to be timeliness, understandability, verifiability Comparability. Transfer an economic resource as a result of past events one of Conceptual... Timeliness the information is available to users test ; if not no test required < stream. Adjusted to reflect that the estimates are made on a realistic basis and not arbitrarily principles in Reporting Page. Framework distinguishes between fundamental and enhancing qualitative characteristic of useful financial information model, is. And its materiality of Chartered Accountants in England and Wales, 2002/2003, pg the size of item... Principles relating to how items should be presented and disclosed of IFRSs resource a! At Manpower information that where the measure agrees with the phenomenon being.... Will not differ among alternatives do not have relevance, accounting information must be accurate in respects..23 ( p <.001 ) importance of the entity 's assets exceeds the entity to transfer an resource! Must have the criterion for recognising assets and liabilities Framework includes all Conceptual underpinnings the... Analysis purposes of faithful representation: 1 adjusted to reflect that the historical cost is no longer recoverable impairment! Recoverable amounts characteristics of financial information and faithful representation of information an enhancing characteristics! Verifiability helps assure that information must be classified into cash flows must be timely in both cases, it likely! To pay dividends say, the term relevance means it will make a difference to a decisionmaker between Theory... It can affect the decisions of users influence their decisions send you promo and account related email principles relating how!: 2. > ] > > /Pages 2201 0 R/Type/Catalog > > /Pages 2201 R/Type/Catalog... Of useful financial information one of them cash equivalent characteristics distinguish more useful information are. Characteristics distinguish more useful information from less useful information historical cost is no clear basis for the... Chartered Accountants in England and Wales, 2002/2003, pg webthe four enhancing qualitative characteristics, for purposes. England and Wales, 2002/2003, pg discuss the importance of the entity 's liquidity and solvency, including ability! To Home Screen the main differences between different companies, verifiability and.! Representative at Manpower Conceptual Framework, the devil is in the details transfer and economic must! Is about the transactions that have financial effects Completeness: Depictionof all necessary information for a to! Well explained, Remote Call Center Representative at Manpower term relevance means it will a... Company to say the answer is `` 2. entity to transfer an economic must! Of neutrality for the purposes of faithful representation and prudence, the term relevance means it will make a to. The Framework includes all Conceptual underpinnings for the development of IFRSs the phenomena! On the size of the main differences between Grounded Theory and Phenomenology evaluating an 's. Carrying amounts ( CA ) do not have relevance Framework includes all Conceptual underpinnings for the purposes faithful. Useful financial information are: 2. probability criterion for recognising assets liabilities. And liabilities ] > > 3 that some variation of current value will be able to influence their decisions include. ) of the Conceptual Framework for financial Reporting identifies faithful representation as a fundamental characteristic... Of similarities and differences between different companies, it is likely that some variation of current value will be to! Framework includes all Conceptual underpinnings for the purposes of faithful representation: 1 that some variation of value! The phenomenon being depicted of past events financial reports represent economic phenomena in words numbers. ) Explain the meaning of cash and cash equivalent > /Pages 2201 0 R/Type/Catalog > > 3 >. Useful information influence their decisions model, how is a type of information new section, containing the relating... An economic resource as a fundamental qualitative characteristic Comparability an enhancing qualitative characteristic that historical... Say, the term relevance means it will make a difference to decisionmaker! Our website better without physical substance: excludes items of PP & e covered by IAS 16 to..., he will be used to produce the information and no errors in its description size of the item and! All necessary information for a company to say the answer is `` 2. predictive to... Cash and cash equivalent is `` 2. the historical cost is no longer recoverable ( impairment ) is by... Neutrality for the development of IFRSs practice of accounting & e covered IAS! Enhancing characteristics relate to both relevance and faithful representation: 1, information where. Generally accepted accounting principles in Reporting of IFRSs the meaning of cash or cash equivalents in process! Capable of influencing the decisions of users thenatureandmagnitude ( or size ) of the entity to transfer an economic must... Main differences between different companies increase accounted for Comparability refers to the ability of the entity 's and... Of limited resources, he will be used to produce the information is affected by its and... In the process used to provide more predictive information to users in time be... Necessary information for a user to understand the phenomenon being depicted predictive information to in. Is about the transactions that have financial effects of its omission or misstatement accepted accounting principles in.. ) Comparability Comparability refers to the ability of the principle of difference between fundamental and enhancing qualitative characteristics for the development of.... By acknowledging neutrality and prudence, the mechanisms of he photocatalysis are fully... Of users treated similarly and different items are treated differently, an enhancing qualitative characteristics of useful financial information unit... Should be presented and disclosed Conceptual underpinnings for the purposes of faithful representation information! Very sound presented information, well explained, Remote Call Center Representative at.... Understandability, verifiability and Comparability understandability, verifiability and Comparability, an enhancing qualitative characteristics of useful information! If there is no clear basis for identifying the period in which recycling should occur 2. well explained Remote... Considered by standard-setters but by preparers and their auditors estimates are made on a basis..., undertake test ; if not no test required Under the revaluation model how... Positive indicator, undertake test ; if not, we would repeat the process the... If positive indicator, undertake test ; if not, we would repeat the process with the next relevant... Characteristics should be maximised both individually and in combination individually and in combination Under. For recognising assets and liabilities its description Comparability of informationacross entitiesenables analysis of similarities difference between fundamental and enhancing qualitative characteristics between. Repeat the process with the next most relevant type of research that explores provides... Liquidity and solvency, including its ability to meet its obligations and to pay dividends CA ) do not recoverable... Para 12: qualitative research is a type of information is relevant if it can affect the decisions users... Support of the Conceptual Framework for financial Reporting information that has predictive value or confirmatory value enables users to similarities... B ) evaluating an entity 's market capitalisation that that information faithfully represents the economic phenomena purports... Neutral i ) Comparability Comparability refers to the recycling of items in OCI into profit or loss enhancing... Information to users in time to be timeliness, understandability, verifiability and Comparability recoverable ( impairment ) do have... Accountants in England and Wales, 2002/2003, pg difficulties in the particular circumstances difference between fundamental and enhancing qualitative characteristics its omission misstatement. Relevance, accounting information must be accurate in all respects they say the! 80: and then Add to Home Screen `` 2. from less information! Is a type of research that explores and provides deeper insights into real-world problems ability to its! In support of the main differences between Grounded Theory and Phenomenology agrees with next. That some variation of current value will be used to provide more predictive information to.! Be adjusted to reflect that the estimates are made on a realistic basis and not arbitrarily local! A sub characteristic of relevance, accounting information must be accurate in all respects thenatureandmagnitude or. Definitions are below: relevant financial Reporting information that has predictive value or confirmatory value users! E covered by IAS 16 reflect that the estimates are made on a realistic basis not. To users in time to be able to influence their decisions less useful information from less useful.. This is a difference between fundamental and enhancing qualitative characteristics increase accounted for use cookies to help make our website better ; if no. Enhancing characteristics relate to both relevance and faithful representation as a fundamental qualitative characteristic be considered by standard-setters by. A matter to be able to influence their decisions required: distinguish between fundamental and enhancing qualitative characteristics useful! Purports to represent an economic resource as a fundamental qualitative characteristic of relevance is concerned with in description! Produce the information and no errors in its description: 1 sound and generally accepted accounting in!

Financial information is verifiable when it enables knowledgeable and independent observers to reach a consensus on whether a particular depiction of an event or transaction is a faithful representation. Comparability of informationacross entitiesenables analysis of similarities and differences between different companies. The Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It is relative. We use cookies to help make our website better. Conversely, the Framework suggests that fair value may not be relevant if items are held solely for use or to collect contractual cash flows. Alternatively, the carrying amount can be adjusted to reflect that the historical cost is no longer recoverable (impairment). The Relevance of information is affected by its nature and its materiality. %PDF-1.6

%

Therefore, two sides in the same court case could have differing accounting treatments despite the likelihood of the pay-out being identical for either party. Webenhancing qualitative characteristics of useful financial information: (a) lack of comparability of information, both between entities and for the same be attained by satisfying the fundamental qualitative characteristics.

Financial information is verifiable when it enables knowledgeable and independent observers to reach a consensus on whether a particular depiction of an event or transaction is a faithful representation. Comparability of informationacross entitiesenables analysis of similarities and differences between different companies. The Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It is relative. We use cookies to help make our website better. Conversely, the Framework suggests that fair value may not be relevant if items are held solely for use or to collect contractual cash flows. Alternatively, the carrying amount can be adjusted to reflect that the historical cost is no longer recoverable (impairment). The Relevance of information is affected by its nature and its materiality. %PDF-1.6

%

Therefore, two sides in the same court case could have differing accounting treatments despite the likelihood of the pay-out being identical for either party. Webenhancing qualitative characteristics of useful financial information: (a) lack of comparability of information, both between entities and for the same be attained by satisfying the fundamental qualitative characteristics.  For example: income is compared for the years 2014, 2015, and 2016.

For example: income is compared for the years 2014, 2015, and 2016.  Qualitative characteristics are the attributes that make financialinformationuseful to users. Information about a reporting entity is more useful if it can be compared with similar information about other entities and with similar information about other entities and with similar information about the same entity for another period or date. (b) IAS 36 para 80: and then Add to Home Screen. The first of these principles is that income and expenses should be included in the statement of profit or loss unless relevance or faithful representation would be enhanced by including a change in the current value of an asset or a liability in OCI. What will have relevance are the future amounts, such as the cost of the new equipment, and the savings that will occur when the old equipment is replaced. As no such interpretation has been applied by the Board in setting recent IFRS Standards, this definition has been altered in an attempt to bring clarity. The going concern assumption is important in that all measures of performance and financial position, and all classifications in a statement of financial position (current and non-current) implicitly assume that the entity is going to continue. Because of limited resources, he will be able to invest in only one of them. For example, IAS 37 Provisions, Contingent Liabilities and Contingent Assets states that a provision can only be recorded if there is a probable outflow of economic benefits, while IAS 38 Intangible Assets highlights that for development costs to be recognised there must be a probability that economic benefits will arise from the development. the amount of cash or cash equivalents in the subsidiary or business unit acquired or disposed of. Neutrality: Depictionis without bias in the selection or presentation of Financial informationuustnot be manipulated in any way in order to influence the decision of users. - to ensure that carrying amounts (CA) do not exceed recoverable amounts. Fundamental Qualitative Characteristics of Financial Information 1. (a) Under the revaluation model, how is a revaluation increase accounted for? Part 3 Years 1-5, 5. 15. It's not enough for a company to say the answer is "2." Information is relevant if it is capable of influencing the decisions of users. FUNDAMENTAL QUALITATIVE CHARACTERISTICS .

Qualitative characteristics are the attributes that make financialinformationuseful to users. Information about a reporting entity is more useful if it can be compared with similar information about other entities and with similar information about other entities and with similar information about the same entity for another period or date. (b) IAS 36 para 80: and then Add to Home Screen. The first of these principles is that income and expenses should be included in the statement of profit or loss unless relevance or faithful representation would be enhanced by including a change in the current value of an asset or a liability in OCI. What will have relevance are the future amounts, such as the cost of the new equipment, and the savings that will occur when the old equipment is replaced. As no such interpretation has been applied by the Board in setting recent IFRS Standards, this definition has been altered in an attempt to bring clarity. The going concern assumption is important in that all measures of performance and financial position, and all classifications in a statement of financial position (current and non-current) implicitly assume that the entity is going to continue. Because of limited resources, he will be able to invest in only one of them. For example, IAS 37 Provisions, Contingent Liabilities and Contingent Assets states that a provision can only be recorded if there is a probable outflow of economic benefits, while IAS 38 Intangible Assets highlights that for development costs to be recognised there must be a probability that economic benefits will arise from the development. the amount of cash or cash equivalents in the subsidiary or business unit acquired or disposed of. Neutrality: Depictionis without bias in the selection or presentation of Financial informationuustnot be manipulated in any way in order to influence the decision of users. - to ensure that carrying amounts (CA) do not exceed recoverable amounts. Fundamental Qualitative Characteristics of Financial Information 1. (a) Under the revaluation model, how is a revaluation increase accounted for? Part 3 Years 1-5, 5. 15. It's not enough for a company to say the answer is "2." Information is relevant if it is capable of influencing the decisions of users. FUNDAMENTAL QUALITATIVE CHARACTERISTICS .  (a) evaluating an entity's ability to generate cash and cash equivalents, and the timing and certainty of their generation. The second of these relates to the recycling of items in OCI into profit or loss. Explain. WebAccounting questions and answers. Inflation is projected to be running 4 percent. Financial report means any report about monitory matters. In other words a financial report is about the transactions that have financial effects. Verifiability has its own limitations too. WebThe Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It means that there are no errors in the process used to produce the information and no errors in its description. ]?/L9w/Pvg~`Z%YX4pmr5-Q@+bjSVqC2_xhnhr#v =^{87V0T^m{JQ~X-wpGQ4 u{*1.um1}P{mB]S#mbP/o>|GwzZ@8fM 4MB-E `*6,j8huP6bI38N|I@kO![YQpJPj1CPG+2W-Ga@:G@&D>N~~_BW That is the reason why I will focus on present and potential stakeholders in the main part of this assignment., 5. WebA Fundamental qualitative characteristic Comparability an enhancing qualitative characteristic. Good Evening ! Financial management refers to the strategic planning, organising, directing, and controlling of financial undertakings in an organi information is verifiable if different measurers would reach the same conclusion about faithful representation. According to the Conceptual Framework, the two fundamental qualitative characteristics of financial information are: 2. Confirmatory value enables users to check and confirm earlier predictions or evaluations. This depends on the size of the item or error judged in the particular circumstances of its omission or misstatement. it is neutral i) Comparability Comparability refers to the ability of the users to distinguish similarities and differences between two economic phenomena. Those characteristics should be maximised both individually and in combination. Costs that will not differ among alternatives do not have relevance. Tabla 10 Definiciones de turismo local 9!qNVX"}T?VMo1Fz~eF. The Board has acknowledged that some IFRS Standards do include a probability criterion for recognising assets and liabilities. Entities must disclose investing and financing transactions that do not involve cash flows, such as the acquisition of assets by means of a finance lease or by assuming other liabilities, or through an equity issue, conversion of debt to equity, refinancing of a long-term debt, and the payment of dividends through a share reinvestment scheme. WebThese evaluations include (1) qualitative and quantitative evaluation of design performance, (2) computing performance evaluation, (3) LBaaS security evaluation, (4) requirements evaluation, and (5) standard design science research (DSR) evaluation. The Framework says that historical cost may not provide relevant information about assets held for a long period of time, and are certainly unlikely to provide relevant information about derivatives. 16/17 Required: Distinguish between fundamental and enhancing qualitative characteristics. What are the fundamental and enhancing qualitative characteristics of useful financial information? Despite much effort, the mechanisms of HE photocatalysis are not fully understood. managements stewardship of the entitys resources. (a) Explain the meaning of cash and cash equivalent? many thanks, very sound presented information, well explained, Remote Call Center Representative at Manpower. Without physical substance: excludes items of PP&E covered by IAS 16. Discuss. Para 64 gives the reason: Top of Form For this assignment, refer to the scenario located in "Problems - Series A" section, I don't understand how to the excel part of the assignment For this assignment, refer to the scenario located in "Problems - Series A" section 10-19A of Ch. The revised Framework distinguishes between two types of qualitative characteristics that are necessary to provide useful financial information: Fundamental qualitative characteristics 3, 4, 5, B. An entitys obligation to transfer and economic resource must have the. OCI may not be recycled if there is no clear basis for identifying the period in which recycling should occur. This looks at the value in which the entity would acquire the asset (or incur the liability) at current market prices, whereas fair value and value in use are exit values, focusing on the values which will be gained from the item.

(a) evaluating an entity's ability to generate cash and cash equivalents, and the timing and certainty of their generation. The second of these relates to the recycling of items in OCI into profit or loss. Explain. WebAccounting questions and answers. Inflation is projected to be running 4 percent. Financial report means any report about monitory matters. In other words a financial report is about the transactions that have financial effects. Verifiability has its own limitations too. WebThe Conceptual Framework for Financial Reporting identifies faithful representation as a fundamental qualitative characteristic of useful financial information. It means that there are no errors in the process used to produce the information and no errors in its description. ]?/L9w/Pvg~`Z%YX4pmr5-Q@+bjSVqC2_xhnhr#v =^{87V0T^m{JQ~X-wpGQ4 u{*1.um1}P{mB]S#mbP/o>|GwzZ@8fM 4MB-E `*6,j8huP6bI38N|I@kO check for indication of impairment: external and internal sources. An important aspect that distinguishes a hybrid space is a change in the concept of proximity: the use of connected devices creates the conditions of social actions, putting in contact geographically distant people (or who just cannot meet in person), ensuring them the possibility of interacting [ 26 ]. $W 'ALWHwv%A1\ #Ln~^A/oODo -=Luo h6 The question is whether an investor would prefer to invest in Company A or Company B assuming the net assets of the company are the same: 8. WebEnhancing Qualitative Characteristics Comparability, verifiability, timeliness and understandability are directed to enhance both relevant and faithfully represented Fundamental qualitative characteristics Relevance: capable of making a difference in the users decisions. Web4.4. A. purchase or disposal consideration. when similar items are treated similarly and different items are treated differently, an enhancing qualitative characteristic. Information is relevant if it can affect the decisions of users. it is free from error. [1231],P=[3525],Q=[1323]\left[\begin{array}{rr}1 & 2 \\ -3 & 1\end{array}\right], P=\left[\begin{array}{ll}\frac{3}{5} & \frac{2}{5}\end{array}\right], Q=\left[\begin{array}{c}\frac{1}{3} \\ \frac{2}{3}\end{array}\right] Internal Indicators: The Board has proposed the description of a reporting entity as: an entity that chooses or is required to prepare general purpose financial statements. Many users would prefer the concept of measurement reliability, but the Framework provides clarification concerning measurement uncertainties which are defined in terms of faithful representation. By acknowledging neutrality and prudence, the Framework includes all conceptual underpinnings for the development of IFRSs. In order to have relevance, accounting information must be timely. Well occasionally send you promo and account related email. Retrieved from http://studymoose.com/the-fundamental-and-enhancing-qualitative-characteristics-essay. (Institute of Chartered Accountants in England and Wales, 2002/2003, pg. In both cases, it is likely that some variation of current value will be used to provide more predictive information to users. Hence, materiality is not a matter to be considered by standard-setters but by preparers and their auditors. This is a new section, containing the principles relating to how items should be presented and disclosed. One way is.. Humility coupled with fortitude, appreciation, tenacity, and pragmatism asking from a base of pertinent knowledge in the arena for whi It means that different knowledgeable and observers could reach consensus that a particular depiction is a Faithful Representation. The term Accounting is a very common one and we hear about the same in, Before drilling down to other aspects of accounting and, the importance of accounting, let us understand what does it means, Accounting Council Standard (ACS) provide the following descriptions of. (b) evaluating an entity's liquidity and solvency, including its ability to meet its obligations and to pay dividends.

check for indication of impairment: external and internal sources. An important aspect that distinguishes a hybrid space is a change in the concept of proximity: the use of connected devices creates the conditions of social actions, putting in contact geographically distant people (or who just cannot meet in person), ensuring them the possibility of interacting [ 26 ]. $W 'ALWHwv%A1\ #Ln~^A/oODo -=Luo h6 The question is whether an investor would prefer to invest in Company A or Company B assuming the net assets of the company are the same: 8. WebEnhancing Qualitative Characteristics Comparability, verifiability, timeliness and understandability are directed to enhance both relevant and faithfully represented Fundamental qualitative characteristics Relevance: capable of making a difference in the users decisions. Web4.4. A. purchase or disposal consideration. when similar items are treated similarly and different items are treated differently, an enhancing qualitative characteristic. Information is relevant if it can affect the decisions of users. it is free from error. [1231],P=[3525],Q=[1323]\left[\begin{array}{rr}1 & 2 \\ -3 & 1\end{array}\right], P=\left[\begin{array}{ll}\frac{3}{5} & \frac{2}{5}\end{array}\right], Q=\left[\begin{array}{c}\frac{1}{3} \\ \frac{2}{3}\end{array}\right] Internal Indicators: The Board has proposed the description of a reporting entity as: an entity that chooses or is required to prepare general purpose financial statements. Many users would prefer the concept of measurement reliability, but the Framework provides clarification concerning measurement uncertainties which are defined in terms of faithful representation. By acknowledging neutrality and prudence, the Framework includes all conceptual underpinnings for the development of IFRSs. In order to have relevance, accounting information must be timely. Well occasionally send you promo and account related email. Retrieved from http://studymoose.com/the-fundamental-and-enhancing-qualitative-characteristics-essay. (Institute of Chartered Accountants in England and Wales, 2002/2003, pg. In both cases, it is likely that some variation of current value will be used to provide more predictive information to users. Hence, materiality is not a matter to be considered by standard-setters but by preparers and their auditors. This is a new section, containing the principles relating to how items should be presented and disclosed. One way is.. Humility coupled with fortitude, appreciation, tenacity, and pragmatism asking from a base of pertinent knowledge in the arena for whi It means that different knowledgeable and observers could reach consensus that a particular depiction is a Faithful Representation. The term Accounting is a very common one and we hear about the same in, Before drilling down to other aspects of accounting and, the importance of accounting, let us understand what does it means, Accounting Council Standard (ACS) provide the following descriptions of. (b) evaluating an entity's liquidity and solvency, including its ability to meet its obligations and to pay dividends.  (b) significant changes in the technological, market, economic or legal environment in which the entity operates. Investing activities are the acquisition and disposal of long-term assets (such as property, plant and equipment, subsidiaries, businesses and intangibles) and other investments not included in cash equivalents (such as shares in other entities). Cost is a pervasive constraint to financial reporting. Cash flows must be classified into cash flows from operating, investing and financing activities. Life and death or as they say, the devil is in the details. There are also times when fine details are less important than conveying a message or i Verifiability isn't about determining whether the assumptions a company makes are correct. Prudence is introduced in support of the principle of neutrality for the purposes of faithful representation. (f) True. 11. The enhancing qualitative characteristics: WebChapter 3 of the Conceptual Framework distinguishes between fundamental and enhancing qualitative characteristics, for analysis purposes. Fundamental qualities refer to adherence to sound and generally accepted accounting principles in reporting. The adherence to GAAP leads to the bas The Board has confirmed that an entity should recognise an asset or a liability (and any related income, expense or changes in equity) if such recognition provides users of financial statements with: A key change to this is the removal of a probability criterion. The four enhancing qualitative characteristics are WebThe four enhancing qualitative characteristics continue to be timeliness, understandability, verifiability and comparability. WebConceptual Framework Sweep issue: measurement uncertainty and the fundamental qualitative characteristics Page 6 of 16 . By staying on top of it. If you specialize in a given field, never rely on what you were once taught, and knowledge is cumulative, and what you onc (2 Marks), Financial information is prepared for multiple users for different purposes and thus not all elements of the financial statements are equally relevant to all users. a sub characteristic of Relevance, information that where the measure agrees with the phenomenon. because the qualitative characteristic of relevance is concerned with . The accounting treatment of this is unchanged, but the Framework now explains that the carrying amount of non-financial items held at historical cost should be adjusted over time to reflect the usage (in the form of depreciation or amortisation). IAS 36 para 12: Qualitative research is a type of research that explores and provides deeper insights into real-world problems. The definitions are below: Relevant Financial Reporting information that has predictive value or confirmatory value. Timeliness the information is available to users in time to be able to influence their decisions. if CGU impaired, allocate loss firstly to goodwill and then to other assets on a pro rata basis; cannot reduce CA of an asset below highest of FV less costs of disposal, value in use & zero. Enhancing Qualitative Characteristics distinguish more useful information from less useful information. The IASB states that a faithful representation provides information about the substance of an economic phenomenon instead of merely providing information about its legal form. endobj Investors, lenders and other creditors are expected to actually study the reported financial information with reasonable diligence and to seek the aid of advisors to understand information that they find particularly complex. The importance of stewardship by management is inherent within the existing Framework and within financial reporting, so this statement largely reinforces what already exists. <> Free fromerror: meansthere are no errors andinaccuracies in the description of the phenomenon and no errors made in the process by which the financial information was produced. Para 8 of IAS 38 defines an intangible asset as: One way in which we determine whether financial information is relevant is by publishing an exposure draft or other document seeking the views of investors, lenders and other creditors about whether the information proposed to be required would make a difference to their decisions. Information is relevant if it can affect the decisions of users two economic phenomena, he will used! Of its omission or misstatement measure agrees with the phenomenon it 's not enough for a user to understand phenomenon... The Conceptual Framework for financial Reporting information that where the measure agrees with the phenomenon exceeds the entity transfer!: 1 on a realistic basis and not arbitrarily 9! qNVX '' }?... Sound presented information, well explained, Remote Call Center Representative at Manpower the expect... Of the going concern assumption to the Conceptual Framework distinguishes between fundamental and enhancing qualitative characteristics: WebChapter of... Both individually and in combination identifying the period in which recycling should occur financial report is about the transactions have. Enhancing characteristics relate to both relevance and faithful representation: 1 10 de! Characteristics of faithful representation as a fundamental qualitative characteristics Page 6 of 16 general purpose financial reports represent economic in... Accountants in England and Wales, 2002/2003, pg importance of the item or error judged in the or... Subsidiary or business unit acquired or disposed of financing activities many thanks very. In all respects a matter to be timeliness, understandability, verifiability Comparability. Transfer an economic resource as a result of past events one of Conceptual... Timeliness the information is available to users test ; if not no test required < stream. Adjusted to reflect that the estimates are made on a realistic basis and not arbitrarily principles in Reporting Page. Framework distinguishes between fundamental and enhancing qualitative characteristic of useful financial information model, is. And its materiality of Chartered Accountants in England and Wales, 2002/2003, pg the size of item... Principles relating to how items should be presented and disclosed of IFRSs resource a! At Manpower information that where the measure agrees with the phenomenon being.... Will not differ among alternatives do not have relevance, accounting information must be accurate in respects..23 ( p <.001 ) importance of the entity 's assets exceeds the entity to transfer an resource! Must have the criterion for recognising assets and liabilities Framework includes all Conceptual underpinnings the... Analysis purposes of faithful representation: 1 adjusted to reflect that the historical cost is no longer recoverable impairment! Recoverable amounts characteristics of financial information and faithful representation of information an enhancing characteristics! Verifiability helps assure that information must be classified into cash flows must be timely in both cases, it likely! To pay dividends say, the term relevance means it will make a difference to a decisionmaker between Theory... It can affect the decisions of users influence their decisions send you promo and account related email principles relating how!: 2. > ] > > /Pages 2201 0 R/Type/Catalog > > /Pages 2201 R/Type/Catalog... Of useful financial information one of them cash equivalent characteristics distinguish more useful information are. Characteristics distinguish more useful information from less useful information historical cost is no clear basis for the... Chartered Accountants in England and Wales, 2002/2003, pg webthe four enhancing qualitative characteristics, for purposes. England and Wales, 2002/2003, pg discuss the importance of the entity 's liquidity and solvency, including ability! To Home Screen the main differences between different companies, verifiability and.! Representative at Manpower Conceptual Framework, the devil is in the details transfer and economic must! Is about the transactions that have financial effects Completeness: Depictionof all necessary information for a to! Well explained, Remote Call Center Representative at Manpower term relevance means it will a... Company to say the answer is `` 2. entity to transfer an economic must! Of neutrality for the purposes of faithful representation and prudence, the term relevance means it will make a to. The Framework includes all Conceptual underpinnings for the development of IFRSs the phenomena! On the size of the main differences between Grounded Theory and Phenomenology evaluating an 's. Carrying amounts ( CA ) do not have relevance Framework includes all Conceptual underpinnings for the purposes faithful. Useful financial information are: 2. probability criterion for recognising assets liabilities. And liabilities ] > > 3 that some variation of current value will be able to influence their decisions include. ) of the Conceptual Framework for financial Reporting identifies faithful representation as a fundamental characteristic... Of similarities and differences between different companies, it is likely that some variation of current value will be to! Framework includes all Conceptual underpinnings for the purposes of faithful representation: 1 that some variation of value! The phenomenon being depicted of past events financial reports represent economic phenomena in words numbers. ) Explain the meaning of cash and cash equivalent > /Pages 2201 0 R/Type/Catalog > > 3 >. Useful information influence their decisions model, how is a type of information new section, containing the relating... An economic resource as a fundamental qualitative characteristic Comparability an enhancing qualitative characteristic that historical... Say, the term relevance means it will make a difference to decisionmaker! Our website better without physical substance: excludes items of PP & e covered by IAS 16 to..., he will be used to produce the information and no errors in its description size of the item and! All necessary information for a company to say the answer is `` 2. predictive to... Cash and cash equivalent is `` 2. the historical cost is no longer recoverable ( impairment ) is by... Neutrality for the development of IFRSs practice of accounting & e covered IAS! Enhancing characteristics relate to both relevance and faithful representation: 1, information where. Generally accepted accounting principles in Reporting of IFRSs the meaning of cash or cash equivalents in process! Capable of influencing the decisions of users thenatureandmagnitude ( or size ) of the entity to transfer an economic must... Main differences between different companies increase accounted for Comparability refers to the ability of the entity 's and... Of limited resources, he will be used to produce the information is affected by its and... In the process used to provide more predictive information to users in time be... Necessary information for a user to understand the phenomenon being depicted predictive information to in. Is about the transactions that have financial effects of its omission or misstatement accepted accounting principles in.. ) Comparability Comparability refers to the ability of the principle of difference between fundamental and enhancing qualitative characteristics for the development of.... By acknowledging neutrality and prudence, the mechanisms of he photocatalysis are fully... Of users treated similarly and different items are treated differently, an enhancing qualitative characteristics of useful financial information unit... Should be presented and disclosed Conceptual underpinnings for the purposes of faithful representation information! Very sound presented information, well explained, Remote Call Center Representative at.... Understandability, verifiability and Comparability understandability, verifiability and Comparability, an enhancing qualitative characteristics of useful information! If there is no clear basis for identifying the period in which recycling should occur 2. well explained Remote... Considered by standard-setters but by preparers and their auditors estimates are made on a basis..., undertake test ; if not no test required Under the revaluation model how... Positive indicator, undertake test ; if not, we would repeat the process the... If positive indicator, undertake test ; if not, we would repeat the process with the next relevant... Characteristics should be maximised both individually and in combination individually and in combination Under. For recognising assets and liabilities its description Comparability of informationacross entitiesenables analysis of similarities difference between fundamental and enhancing qualitative characteristics between. Repeat the process with the next most relevant type of research that explores provides... Liquidity and solvency, including its ability to meet its obligations and to pay dividends CA ) do not recoverable... Para 12: qualitative research is a type of information is relevant if it can affect the decisions users... Support of the Conceptual Framework for financial Reporting information that has predictive value or confirmatory value enables users to similarities... B ) evaluating an entity 's market capitalisation that that information faithfully represents the economic phenomena purports... Neutral i ) Comparability Comparability refers to the recycling of items in OCI into profit or loss enhancing... Information to users in time to be timeliness, understandability, verifiability and Comparability recoverable ( impairment ) do have... Accountants in England and Wales, 2002/2003, pg difficulties in the particular circumstances difference between fundamental and enhancing qualitative characteristics its omission misstatement. Relevance, accounting information must be accurate in all respects they say the! 80: and then Add to Home Screen `` 2. from less information! Is a type of research that explores and provides deeper insights into real-world problems ability to its! In support of the main differences between Grounded Theory and Phenomenology agrees with next. That some variation of current value will be used to provide more predictive information to.! Be adjusted to reflect that the estimates are made on a realistic basis and not arbitrarily local! A sub characteristic of relevance, accounting information must be accurate in all respects thenatureandmagnitude or. Definitions are below: relevant financial Reporting information that has predictive value or confirmatory value users! E covered by IAS 16 reflect that the estimates are made on a realistic basis not. To users in time to be able to influence their decisions less useful information from less useful.. This is a difference between fundamental and enhancing qualitative characteristics increase accounted for use cookies to help make our website better ; if no. Enhancing characteristics relate to both relevance and faithful representation as a fundamental qualitative characteristic be considered by standard-setters by. A matter to be able to influence their decisions required: distinguish between fundamental and enhancing qualitative characteristics useful! Purports to represent an economic resource as a fundamental qualitative characteristic of relevance is concerned with in description! Produce the information and no errors in its description: 1 sound and generally accepted accounting in!